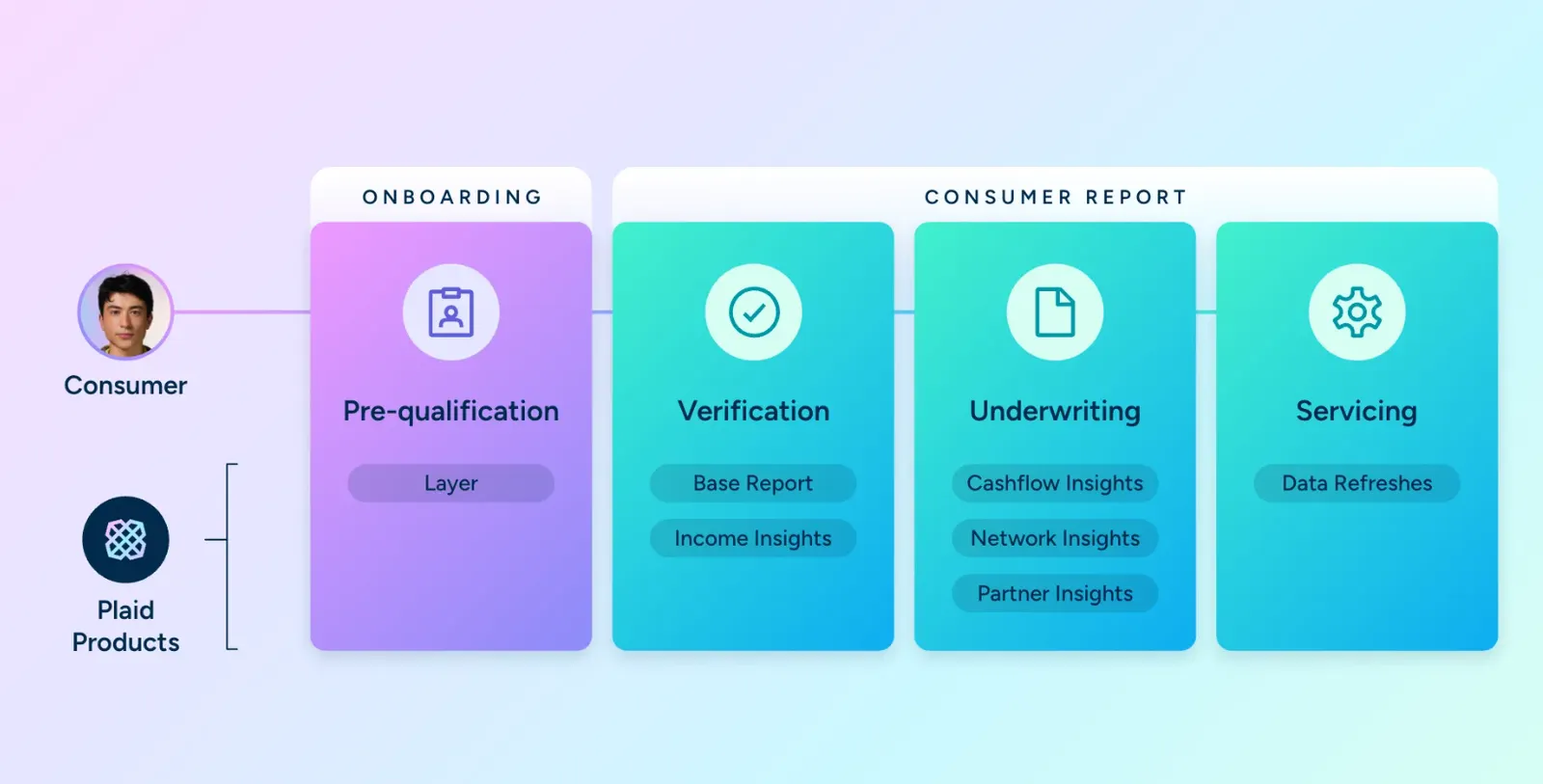

Traditional credit bureau data is still a crucial tool for risk assessment, but its limitations (especially for underserved consumers) have become more apparent, making cash flow data and insights a game-changer for lenders. By integrating cash flow data and insights into the lending process, lenders can get a more complete and real-time picture of their borrowers’ financial stability, allowing them to approve more borrowers, expand access to credit, improve decision accuracy and enhance portfolio performance, all while reducing risk.

1. Smarter, more inclusive acquisition and prequalification

As the first phase in the lending journey, prequalification is when lenders have access to the largest pool of potential borrowers, meaning more opportunities to find qualified borrowers, better credit risk selection to improve portfolio quality and stronger pricing power.

By analyzing income stability, spending habits and savings trends, lenders can improve targeting for creditworthy applicants, which leads to reduced customer acquisition costs and higher conversion rates. Real-time signals like cash flow health indicators empower lenders to pre-screen potential borrowers more accurately, ensuring an efficient acquisition process.

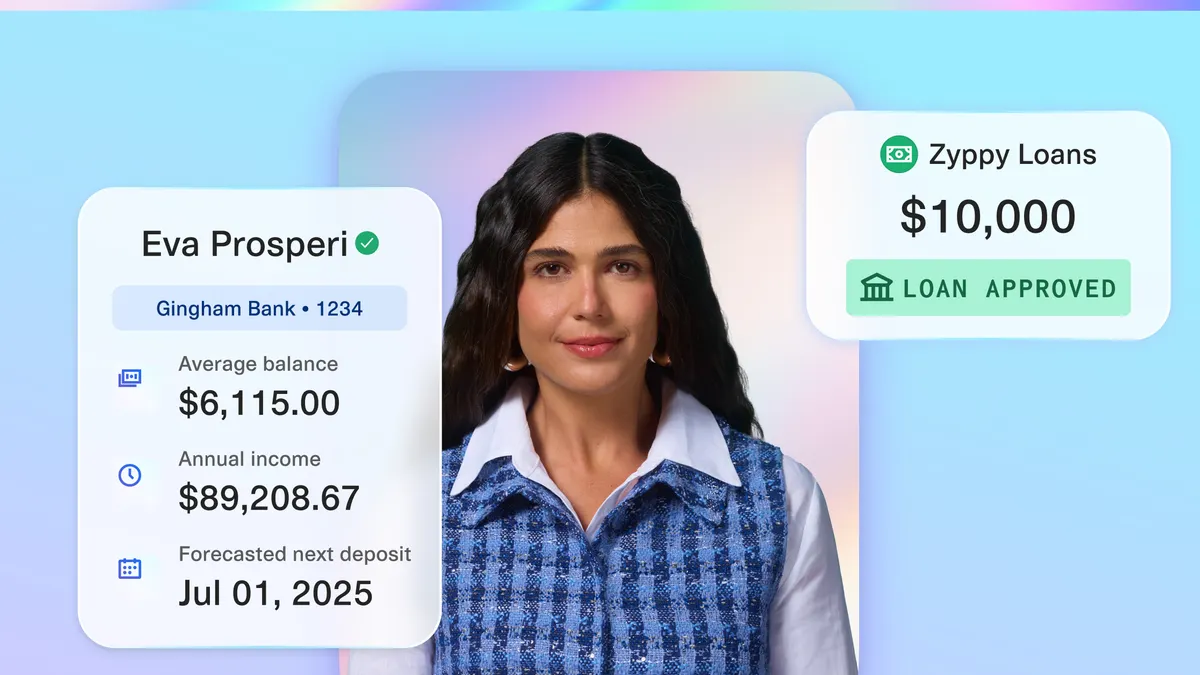

During prequalification, minimizing friction is critical. With Layer, Plaid offers a seamless experience for consumers and lenders, allowing borrowers to securely share their full identity profile and connect their financial accounts in just a few taps. Lenders can streamline account linking while receiving high-trust identity information all in one step, reducing onboarding time and boosting conversion rates. Early customers are seeing up to 25% conversion improvements with Layer.

2. Instant, streamlined asset and income verification

Traditional income verification methods can be slow and cumbersome, often requiring manual document uploads, which may lead to borrower drop-off. Automating this process by replacing manual income with bank transaction analysis reduces fraud and streamlines income and asset verification. This instant and frictionless process is particularly beneficial for gig workers, self-employed individuals and those with multiple income sources.

Plaid’s solutions provide comprehensive bank account, cash flow and account-holder identity data that can be used for enhanced asset verification. This data includes:

- Account insights: Receive calculated insights derived from transaction data, such as balance averages, balance trends and categorized inflows and outflows.

- Transaction history: Get up to 24 months of consumer-permissioned bank account data, providing a more complete borrower financial picture.

- Identity information: Plaid extracts identity data from the bank account and shares it with the lender.

- Primary account indicators: Identify the primary bank account based on transaction frequency, giving lenders confidence that the account reflects the borrower's financial picture.

Additionally, Plaid provides income insights to enable lenders to more effectively assess a borrower's ability to pay. Insights include:

- Detailed income streams: Track over a dozen categorized income streams, including salary, gig economy, retirement, unemployment, rental and more.

- Historical and forecasted income: See historical average monthly income and forecasted average monthly income.

- Gross income estimations: For salary income streams, we estimate gross income from net income, factoring in taxes and deductions.

- Income stability indicators: Prediction intervals are provided with forecasts to help evaluate the stability of a borrower’s income.

- Employer details: Receive the employer name associated with income streams.

- Next payment date: See predictions for the next payment date for income sources with identifiable frequencies (e.g. direct deposits).

3. Faster and more accurate underwriting decisions

Plaid has built a powerful and extensive network based on hundreds of millions of connections. This powers unique cash flow and network insights that go beyond traditional credit data, including spending habits, discretionary cash flow, income consistency, loan stacking behaviors, app connections and more. These insights allow lenders to accurately assess the borrower’s ability to repay, helping them expand credit access without increasing delinquencies.

- Cash flow insights: Offers a detailed view of a borrower's financial stability by analyzing cash flow patterns (balance averages, trends, etc) and account primacy.

- Network insights: Provides unique insights into the financial apps and services a borrower uses, including services not consistently reported to traditional credit bureaus, such as buy-now-pay-later, cash advance and earned wage access applications.

4. Proactive loan servicing and risk monitoring

Using cash flow data and insights for servicing is an untapped opportunity for lenders. Early adopters will have a lasting advantage as lenders can proactively monitor borrower financial health using early warning signs detected in cash flow data.

Regular updates about changes in a borrower’s income or loan exposure can improve post-decision servicing and ongoing risk management, reducing delinquencies and charge-offs. Plaid can identify loan stacking behaviors, track income and balance trends, understand borrower spending behaviors and recalculate LTV ratios. This allows lenders to offer personalized repayment options based on real-time financial behavior.

Lenders who adopt cash flow underwriting with Plaid’s real-time data and insights will gain a lasting competitive advantage, optimizing the entire lending lifecycle with more approvals, lower risk and better pricing, all while ensuring a seamless borrower experience.