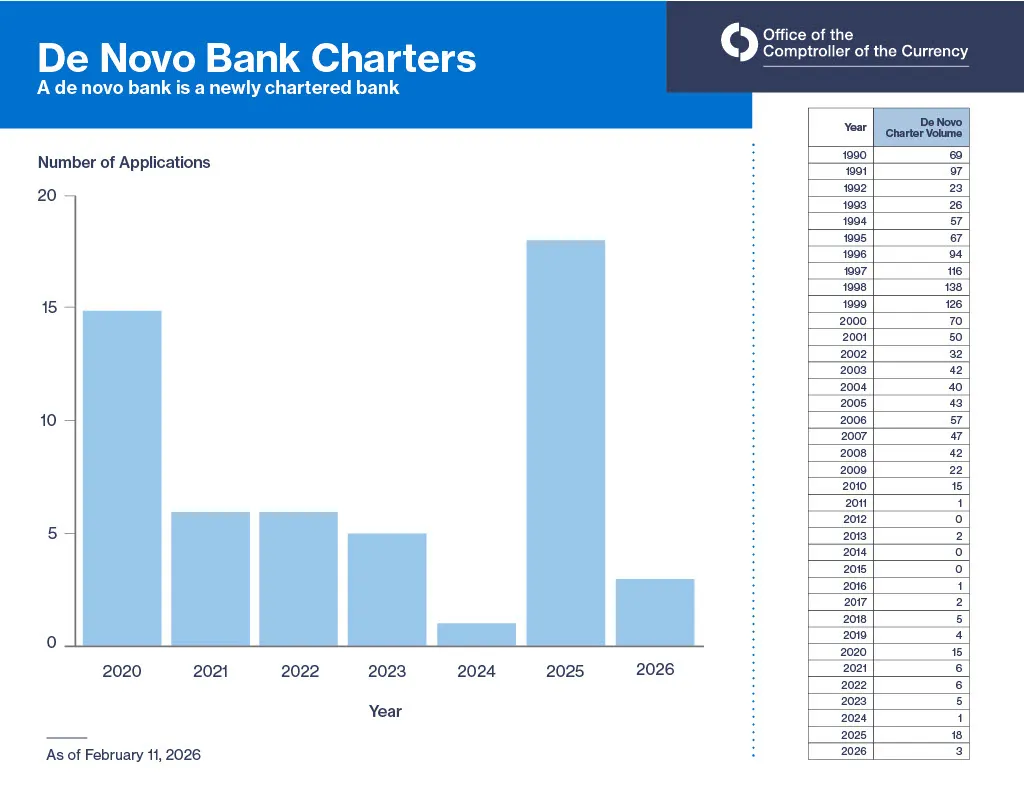

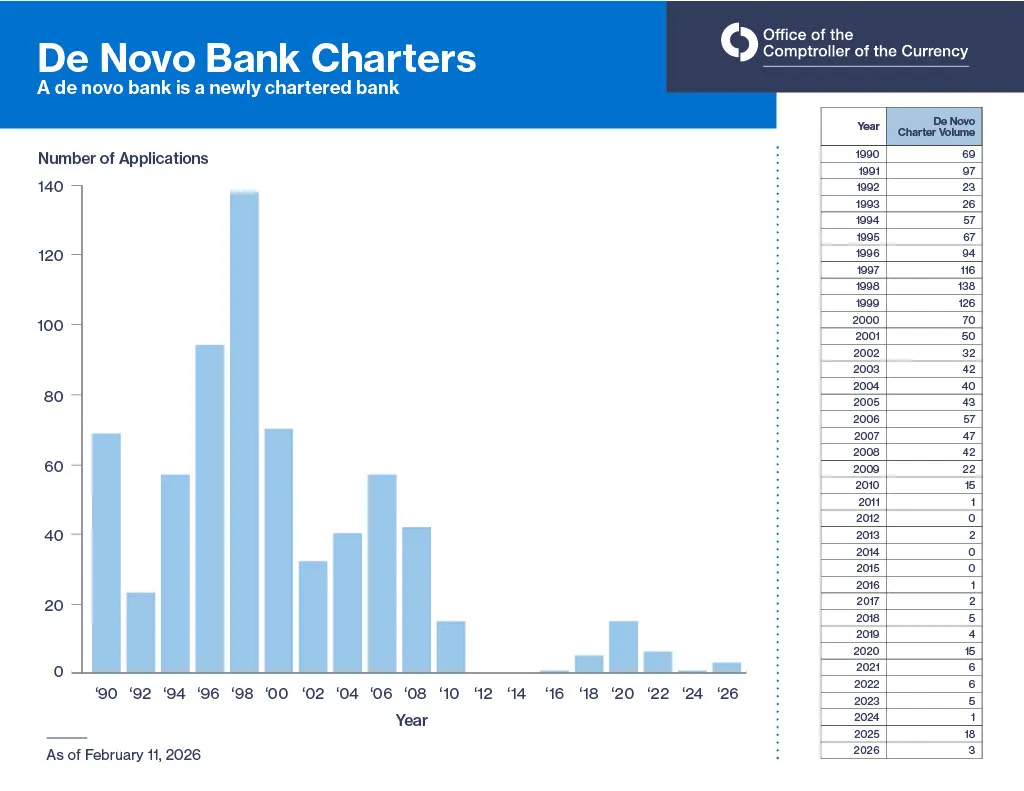

Bank charter applications exploded last year to a level not seen since 2008.

The 18 bank charter applications submitted to the Office of the Comptroller of the Currency in 2025 equaled the number received in the prior four years combined.

In December, Jonathan Gould, the agency’s chief, called the application boom “a return to the norm.”

But nearly every year between 1990 and 2008 saw at least double 2025’s number of charter applications, including a sevenfold peak in two of those years.

In an interview this month, Gould said he doesn’t “presume to know what the, or whether there is, an ‘appropriate’ level of interest or not.”

Generally, “new bank formation in this country is a sign of the health of the banking system,” he said. “And it is something that, where possible and consistent with the statutory factors, we should encourage, because it is a way to ensure that the banking system remains responsive to the communities and the economies across America that it is designed to serve.”

Following the 2007-08 financial crisis, the agency’s appetite for new bank charters fell off a cliff, Gould noted – wording that dovetails with fellow Trump-era regulator Travis Hill, who leads the Federal Deposit Insurance Corp.

Many of the banks that faltered in the financial crisis – Lehman Brothers, Washington Mutual (acquired by JPMorgan Chase), Wachovia (scooped up by Wells Fargo) – were not newly chartered but rather were well over 100 years old. Nonetheless, the charter slump mirrored a reduced risk tolerance in the banking system after 2008.

“You see it in a whole host of other areas – in terms of our regulation and supervision, too,” Gould said. “This is just one, to me, very important aspect that uniquely affects the OCC because we are the sole chartering authority at the federal level.”

Gould served as the agency’s chief counsel from 2018 to 2021. He was nominated to lead the OCC in February 2025, and confirmed in July. He’s been intent on elevating the agency’s chartering arm since his return.

Ace in hand

Six months ago, Gould took what was then called the licensing group, dubbed it the chartering organization and structure team, and changed the unit’s chain of command so that it reported directly to him.

It has a “critical importance to the federal banking system,” Gould said, “as, in some sense, the gatekeepers of the system.”

The chartering organization is run by OCC lifer Stephen Lybarger, who joined the agency fresh out of college in 1984. By 2010, he was a senior executive in the department, and last year was promoted to senior deputy comptroller. Many people on his team have likewise spent years at the OCC.

The agency’s headcount fell by 216 late last winter, between probationary employee layoffs and voluntary resignations, according to a memo seen by Bloomberg Law.

Gould did not share how many employees left the chartering function, but he told Banking Dive the smaller headcount has “caused us to look more critically at how we allocate resources and make sure that we are using our skilled employees to their highest and best use.”

Gould’s ace in the hand, though, is a system he set up during his previous stint at the OCC: a mechanism for rotations from the supervision arm into the chartering organization, which ensures “a real pipeline of talented people.”

Examiners are pulled from supervision into one- to two-year rotations within the chartering arm, and that unit “get[s] the benefit of skilled and capable examiners wearing a slightly different hat from their normal day-to-day roles” who can face an increase in chartering interest head-on.

When the mechanism was created, leaders within the chartering function were aging, and the change allowed for a “next generation pipeline,” Gould said.

Given that several of 2025’s 18 charter applications have gained conditional approval, with one (Erebor) already open as a bank, the chartering arm – and its pipeline – may be in full swing.

Opposition

Not everyone sees the influx of charter applications in the same light as Gould – particularly with regard to national trust charters, which allow financial institutions to perform fiduciary duties and custodial services without taking deposits or making loans.

Bank trade groups such as the American Bankers Association and advocacy organizations such as the Bank Policy Institute have urged the OCC to pump the brakes on national trust charters sought by cryptocurrency firms.

Critics are concerned that the approval of charters for crypto firms, many of which intend to issue stablecoins and custody digital assets, while the federal crypto framework is incomplete, is too risky.

Other groups, like the Conference of State Bank Supervisors, take issue with the OCC’s recent proposal to amend chartering regulation language to clarify that national trust banks are not limited to fiduciary activities.

But the CSBS alleges a change in language “would instead create uncertainty and could result in serious implications by overstepping National Bank Act authority.”

The Financial Technology Association, which represents fintech firms, agrees with the proposed language change.

Gould declined to comment on the language change, which is up for public comment.

The comptroller will see you now

The OCC announced plans to change its community bank examination procedures in October, and for some banks that have undergone an exam of late, that’s included an unexpected guest: Gould himself.

The comptroller recently started accompanying examiners, and it’s been a “hugely valuable experience” for him to see examiners in action and talk directly with community bankers, he told Banking Dive.

“That has directly informed the supervision and regulatory reform efforts that we are making at the OCC to assist community banks and relieve them of some of the unnecessary burdens to which they have been subjected over the years, particularly in the years following the Dodd-Frank Act, that are not consistent with the risks presented by a community bank engaged in traditional community bank banking activities,” he said.

Gould, who is not a bank examiner, said he’s not there during the entirety of a multiweek exam. But he said it’s a unique opportunity to “get feedback directly from the bankers on what they are seeing, whether in connection with our supervision of them, or just more broadly in the communities in which they're operating.”

The OCC under Gould has made several changes to community bank supervision, including reducing the rates in the general assessment fee schedule by 30% for banks with up to $40 billion in assets and amending its guidance such that community banks have the flexibility to tailor model risk management practices in conjunction with the bank’s risk exposures, business activities, and the complexity and extent of its model use.

Some proposed changes, such as a reduction in the community bank leverage ratio, have been well-received by bank trade groups. At least one proposal, however – a simplified Community Reinvestment Act strategic plan – has drawn ire for its potential to result in less financing devoted to affordable housing, community development financial institutions and economic revitalization.

All told, Gould said he wants the changes to enable banks over time “to be measured not on the size of their regulatory teams, but rather on the strength of the services they provide to their local communities.”